The Cost of Compute 2026

How 100 CFOs are approaching cloud costs in 2026.

Cloud Infrastructure Accounting Standards

GAAP-aligned principles for cloud and AI cost classification.

CFO Classification Handbook

A practical framework for classifying cloud and AI costs.

Practical guides for cloud-aware finance teams.

Report

The Cost of Compute 2026

What 100 CFOs revealed about cloud costs and how it impacts their P&Ls.

Get the reportGAAP doesn’t define SaaS COGS — it defines costs necessary to satisfy the promised service, and SaaS companies call that COGS.

If implementation and onboarding costs are required to get a customer up and running, they must be included in COGS. The problem is, these costs don’t behave like other COGS; they are not ongoing; they behave more like sales commissions than hosting expenses.

In many modern SaaS businesses, a large share of implementation costs is infrastructure: initial data loads, provisioning dedicated environments, or pre-purchasing cloud storage and data. Those are front-loaded COGS tied to new contracts, not to the recurring service. Treating them like run-rate hosting costs can badly misrepresent your cloud unit economics.

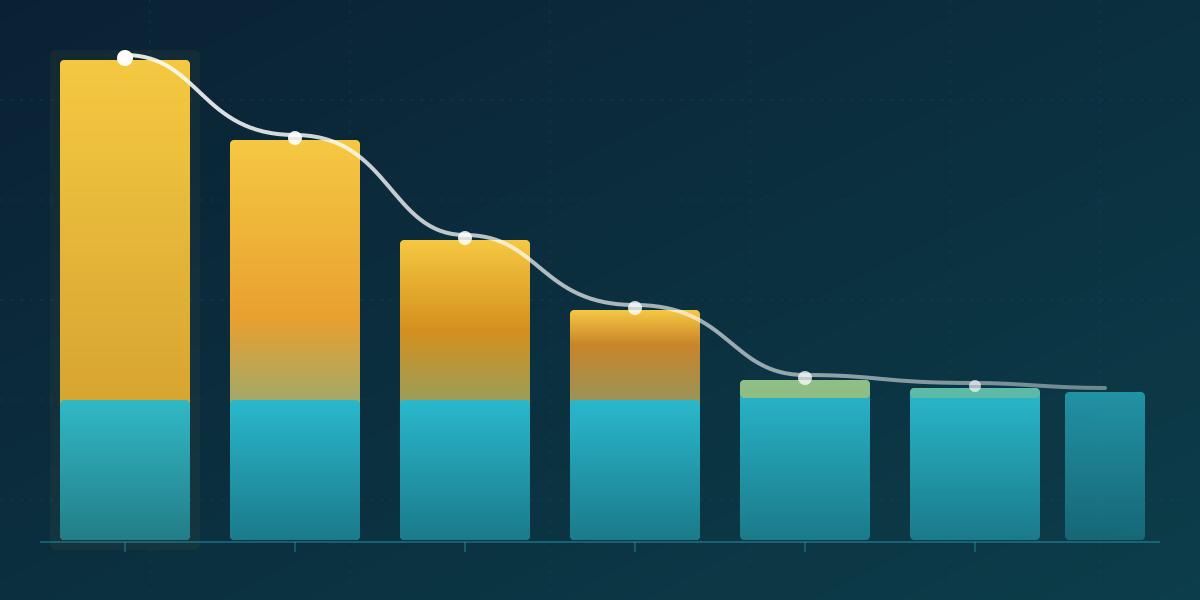

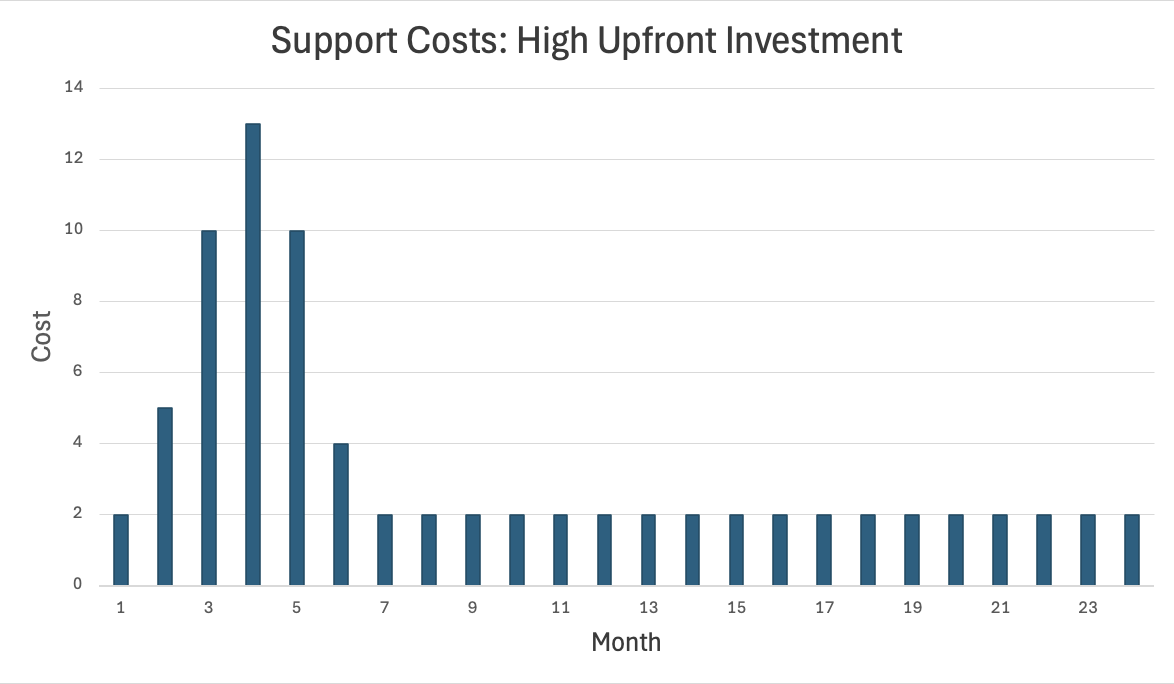

If your costs to support a customer look like the chart below, you should capitalize onboarding/implementation costs.

Why?

First, GAAP says you should. This is not my favorite reason, as I oppose capitalizing software development in almost all circumstances, but here it makes sense.

Second, and most importantly, capitalization gives a clearer picture of the company’s financial performance. Without capitalization, new customer growth depresses gross margins below their long-term averages. Higher growth increases the ratio of new customers to mature customers, thereby temporarily inflating costs. This distortion affects unit-level economic metrics such as the CAC Ratio and the LTV-to-CAC Ratio, making the business appear less profitable and economically viable than it is.

Managers and investors are comfortable front-loading sales and marketing expenses to drive growth at the expense of profits, but up-front COGS spending gets buried in the P&L, and is not something managers or investors can adjust for on their own.

I’m currently working with a young, growing SaaS business that has a negative gross margin due to the up-front implementation costs referenced above. Negative gross margins are normally an existential threat to a company, but in this case, it’s a timing difference masking strong unit economics. They are looking to raise some capital, which will be impossible if they don’t fix their accounting.

If implementation and onboarding costs are dragging down your gross margin by more than a few percentage points, you should explore capitalizing them. (ChatGPT can tell you how.)

If a CFO presented this approach to me as a board member, I would favor the move, but with two caveats. One, keep me informed on cash. This P&L presentation will understate cash burn, and must be accompanied by a cash-flow statement. Second, it should be used only when growth depresses margins, not as a temporary gross margin boost for a low-growth business.

Report

Download The Cost of Compute 2026

Cloud Capital earns a share of the savings we generate for you. If you don't save, we don't get paid. Our incentives are fully aligned with yours. Ready to take control of your cloud spend?