The Cost of Compute 2026

How 100 CFOs are approaching cloud costs in 2026.

Cloud Infrastructure Accounting Standards

GAAP-aligned principles for cloud and AI cost classification.

Economics of AI Infrastructure

How AI workloads break traditional SaaS unit economics.

Practical guides for cloud-aware finance teams.

Report

The Cost of Compute 2026

What 100 CFOs revealed about cloud costs and how it impacts their P&Ls.

Get the reportTodd Gardner is a US-based capital formation and valuation expert. He has funded over 100 SaaS companies and currently serves as managing director at SaaSonomics.

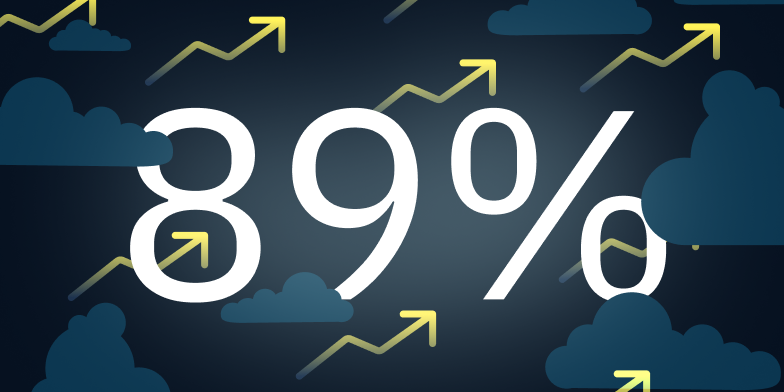

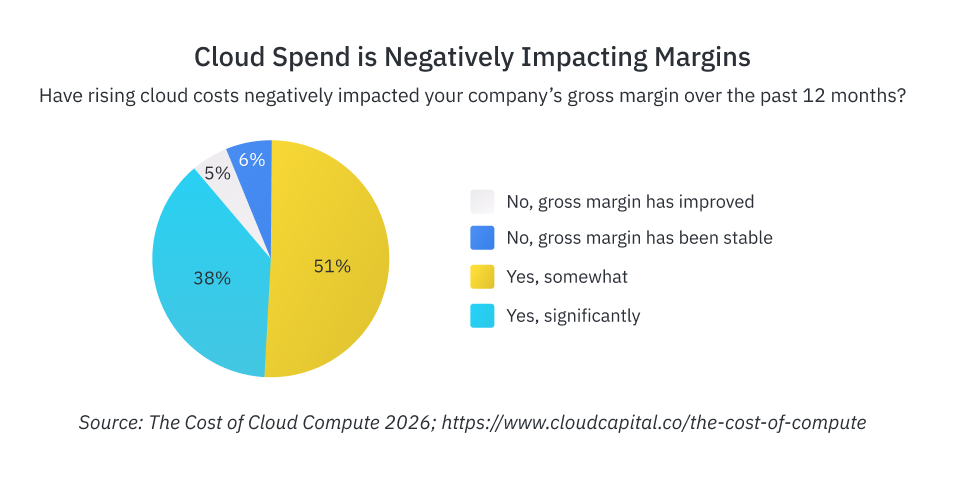

In a recent survey of 100 SaaS CFOs by Cloud Capital, 89% reported that rising cloud costs negatively impacted gross margins.

In some cases, new AI development efforts have increased cloud costs. For others, traditional workloads are costing more because of AI-driven pricing pressure. Either way, declines in gross margin are putting significant pressure on SaaS valuations.

Let's unpack exactly why and how much.

The first step in understanding the role of gross margins in SaaS valuations is to forget SaaS valuations before 2021. Before 2021, the space was emerging, growing quickly, and investors assumed companies could transition to profitability in the future. This was rational at the time, and when growth slowed, valuations shifted from multiples of revenue to multiples of profit. During the revenue-multiple era, if your company had a "normal" gross margin, a few points one way or the other was not material in its valuation.

Now, however, because gross margins directly impact profits, they also directly impact valuations, and in a substantial way. Let's look at current public SaaS data to demonstrate.

The median gross profit margin of public SaaS companies is currently 78%, and the median operating profit is 18%. Hypothetically, if gross margins were to drop by five percentage points for a billion-dollar company, operating profit would fall from $180 million to $130 million. The decline in profits would be destructive to the company's valuation for three reasons.

First is the simple math with a constant PE multiple of 30 (which is pretty close to the current median).

$180 million X 30 = $5.4 billion

$130 million X 30 = $4.0 billion

So, with a constant multiple, the valuation decreases by 25% given a 5-point decline in gross margins.

Second, since investors focus more on future earnings than on current earnings, and this company's earnings are shrinking, it's likely that its P/E ratio would drop dramatically below 30.

Third, COGS matter more to investors than operating expenses. Given the same level of operating profit, high-gross-margin companies are worth more. Why? COGS are variable expenses that are hard to cut without immediate negative consequences. New methods and efficiencies must be found to reduce COGS, and that's more difficult than cutting operating expenses to drive profits.

This example is a gross simplification, but it's still important to understand the basic math SaaS companies face. If a business is making big bets on AI, it might be able to explain away the gross margin decline, but only if it can back it up with data isolating core gross margins from development costs. (more on this in future posts)

As a core driver of profits, gross margins are a massive driver of a SaaS company's valuation, and they are headed in the wrong direction. Maintaining or improving gross margins in this environment needs to be on every CFO's radar.

Report

Download The Cost of Compute 2026

Cloud Capital earns a share of the savings we generate for you. If you don't save, we don't get paid. Our incentives are fully aligned with yours. Ready to take control of your cloud spend?